Week 17...

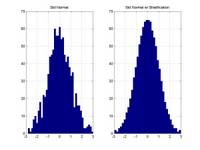

So there is a method to the madness. The idea of Monte Carlo simulation for pricing derivatives is well known, but even more fascinating are the mathematical constructs to speed up the process. The basic normal random number generators cluster the points in space, but quasi-random sequences (QRS) and stratification techniques help make the process more efficient. An excellent online java applet to visualize this is given here.

Week 17 - credit final .. and paper was due.

Monte Carlo using Stratification

Week 17 - credit final .. and paper was due.

Monte Carlo using Stratification

posted by Quantjock at 1:36 AM

![]()

3 Comments:

Hi Swaroop,

I read up on Aloke's blog and have spoken to him also. I noticed your post Derman below, and our firm was actually named way back in the day in his book.

MM (quantrecruiter.com)

edit: "on Derman's blog below"...

thanks.. I just saw your blog.. pretty cool

Post a Comment

<< Home